News Markets & Companies

Challenges ahead: an update on the European decorative paint market

The European decorative paint market remains challenging. However, there are some positive signs that the economic environment may improve. The construction sector is still under pressure, and DIY consumers are more price-sensitive than before the pandemic. For 2025, the decorative paint market in Europe is expected to remain flat. By Douglas Bohn, Orr & Boss Consulting

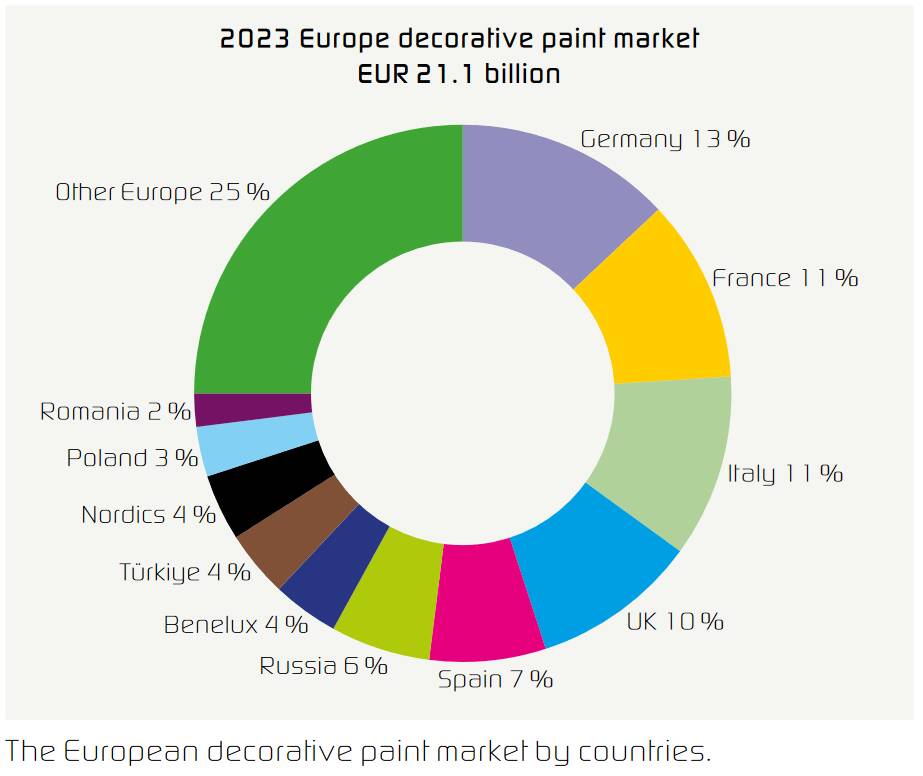

In 2023, the European paint market is estimated at around 4.5 billion litres and EUR 21.1 billion. Germany, France, Italy, the UK, and Spain are the leading markets. Since early 2022, the downturn has shifted country shares. Germany remains the largest decorative paint market in Europe but has weakened due to a sharper decline in the local construction market compared to other countries. Italy and Spain have benefited from stronger construction activity, increasing their share of the total market. The five largest markets – Germany, France, Italy, the UK, and Spain – still account for more than 50% of the European decorative coatings market.

The breakdown between DIY and professional segments varies by country. On average, the DIY share is around 35%, slightly higher in Germany and France, and somewhat lower in Poland, other Eastern European markets, and countries like Portugal. The market environment has been difficult for the past two and a half years. Since its peak in 2021, the volume has dropped by around 15%.

Construction Market

The decline has not been uniform across Europe. Germany has seen the sharpest drop, while Italy, Spain, Portugal and others have fared better. The overall decline is largely driven by falling construction activity. The first chart shows an EU construction index, which indicates a nearly continuous decline since February 2022. Although some stabilisation has occurred recently, the index remains well below early 2022 levels.

Country Trends

The construction sector has been hit hardest in Germany, France, and Poland, while Southern European countries such as Spain, Portugal, and Italy have shown slight growth. New builds are not the only factor affecting the decorative paint market. The DIY segment and the contractor repaint market are closely linked to consumer sentiment. Inflationary pressures and high interest rates have made households more cost-conscious, leading to reduced spending on paint in some countries.

Germany: Market conditions remain difficult. Strong growth during the 2010s has resulted in a steeper decline now. High prices and interest rates continue to dampen consumer spending and construction. Decorative paint volume in Germany is estimated to have fallen by about 25% since the 2021 peak.

France: The construction sector in France continues to struggle. Lower building activity and declining consumer confidence have impacted both new builds and renovations. A volume drop of 2–4% was estimated for 2023, with a similar decline likely in 2024.

Spain and Portugal: The Iberian decorative paint market rebounded slightly in 2023 after a dip in 2022. Construction and building indices showed moderate growth, supporting slight improvements in Spain and Portugal.

Italy: Growth was previously driven by government incentives for façade renovations. These ended in 2023, but a slight positive trend continues.

UK: Volume was estimated to be down 2% in 2023 and has remained nearly flat in 2024 so far.

Outlook

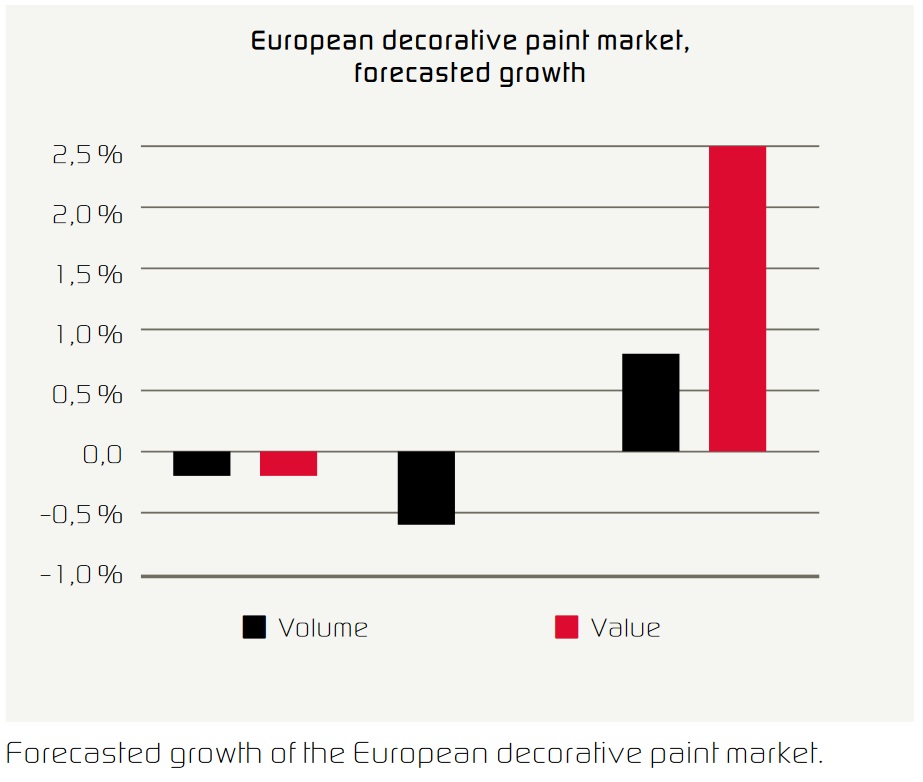

Inflation is easing, and interest rates have started to fall. The European Central Bank has already lowered rates once, with further cuts expected. These changes could help normalise market conditions and gradually boost construction activity. However, only a modest rebound is likely, and it will take years to recover the 15% volume lost since 2021. Assuming further interest rate cuts, average annual volume growth of around 0.8% is projected for the European decorative paint market through 2029.

Conclusion

The past three years have been challenging. The outbreak of the Ukraine war, the 2022 energy crisis, and interest rate hikes led to a 15% drop in volume compared to 2021. Most of the downturn appears to be over. Southern European markets such as Italy, Spain, and Portugal are starting to grow again, while construction remains weak in Germany, France, Poland, and other countries. Further interest rate cuts could help the construction sector in these markets recover.